Aerospace and Defence Industry

About the Sector

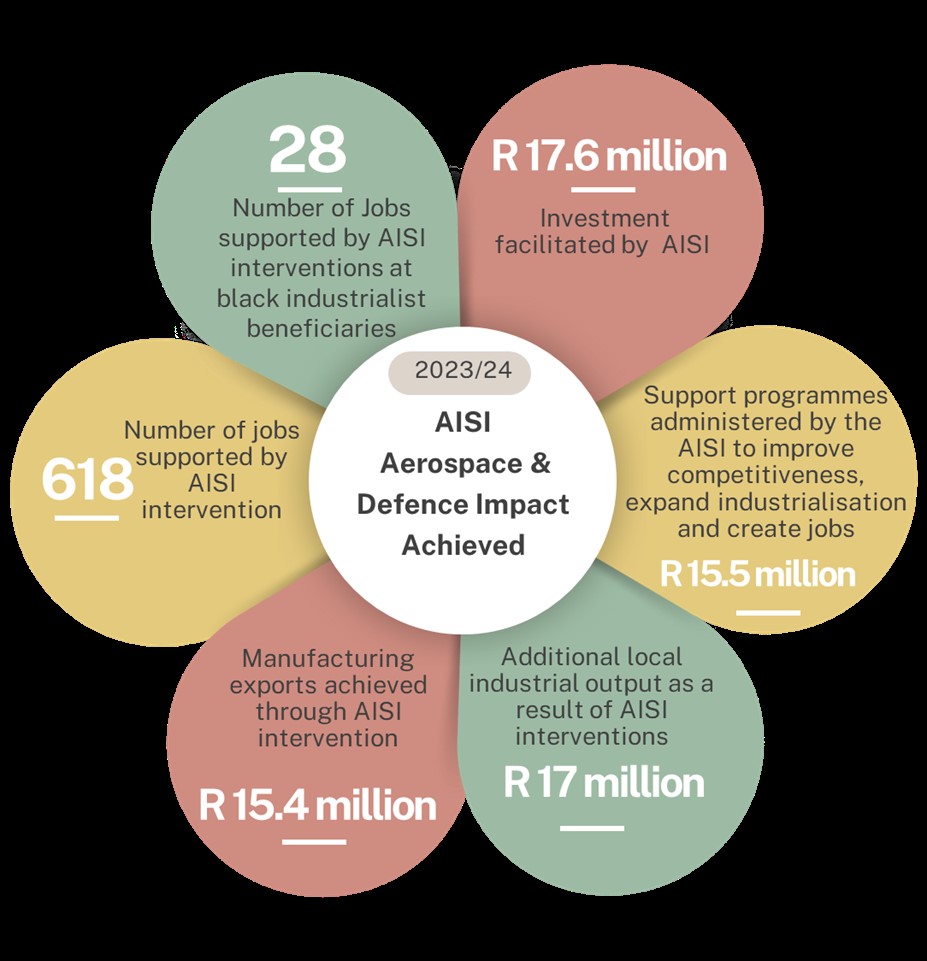

The South African Aerospace and Defence industry is a globally competitive industry that supports national interests and is striving to be the preferred choice for aerospace and defence-related solutions on the African continent. The industry’s revenue is constrained by politics and government budgets. Consequently, it continues to develop technologies for defence use while also branching into civil applications. the dtic, through its Aerospace Industry Support Initiative (AISI), continues to provide tailored financial and technical support to the aerospace and defence industry.

Key constraints

- The primary risk facing the industry is the continued underfunding of the South African National Defence Force, which restricts its ability to acquire new equipment and systems, and to support new research and development. While several companies have done well in the export market, considerable future potential will be lost if the industry does not have new products with which to compete.

- The second greatest risk lies in export controls that are both slow and erratic. This can discourage repeat orders and even deter potential clients.

- There is also limited industrial and financial support.

- Power cuts due to loadshedding within the country affected many businesses, resulting in low production that has affected profits and resulted in people losing jobs.

Key opportunities

- Positioning the local industry as a one-stop-shop that provides defence solutions for the African continent, and as a preferred African partner.

- Maintenance, refurbishment and overhaul of aerospace and defence products.

- Promote job creation and skills transfer by developing new technologies and increasing opportunities to establish more companies.

Progress highlights

- Boosting Black-Women Owned SMME: Advancing Pressure Testing & ISO 9001 Certification Intervention

Contact Details

Ms Nokwanda Fipaza

Director: Aerospace and Defence

Tel: +27 (0)12 349 5567

E-mail: NFipaza@thedtic.gov.za